[ad_1]

Whoa, have you ever seen what simply occurred to rates of interest!?

All of the sudden, after not less than fourteen years of our monetary world being largely the identical, anyone flipped over the desk and now issues are fairly completely different.

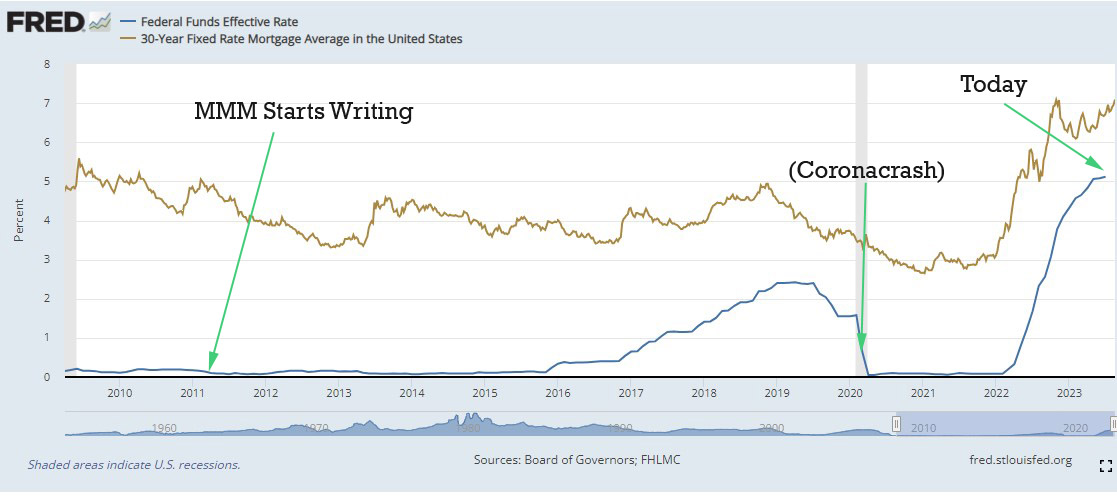

Rates of interest, which have been gliding alongside at near zero since earlier than the Daybreak of Mustachianism in 2011, have immediately shot again as much as 20-year highs.

–

Which brings up a couple of questions on whether or not we have to fear, or do something about this new growth.

- Is the inventory market (index funds, in fact) nonetheless the precise place for my cash?

- What if I need to purchase a home?

- What about my present home – ought to I cling onto it eternally due to the solid-gold 3% mortgage I’ve locked in for the subsequent 30 years?

- Will rates of interest maintain going up?

- And can they ever return down?

These questions are on everyone’s thoughts lately, and I’ve been ruminating on them myself. However whereas I’ve seen loads of play-by-play tales about every little rate of interest improve within the monetary newspapers, none of them appear to get into the essential half, which is,

“Yeah, rates of interest are manner up, however what ought to I do about it?”

So let’s discuss technique.

Why Is This Taking place, and What Bought Us Right here?

Rates of interest are like an enormous fuel pedal that revs the engine of our financial system, with the polished black costume shoe of Federal Reserve Chairman Jerome Powell pressed upon it.

For many of the previous twenty years, Jerome’s workforce and their predecessors have stored the pedal to the steel, firing a extremely flamable stream of straightforward cash into the system within the type of near-zero charges. This made mortgages extra inexpensive, so everybody stretched to purchase homes, which drove demand for current houses and new building alike.

It additionally had the same impact on enterprise funding: borrowed cash and enterprise capital was low cost, so plenty of entrepreneurs borrowed plenty of cash and began new corporations. These corporations then rented workplaces and constructed factories and employed staff – who circled again to purchase extra homes, vehicles, fridges, iPhones, and all the opposite luxurious facilities of contemporary life.

This was an ideal get together and it led to plenty of good issues, as a result of we had twenty years of prosperity, development, elevating our kids, inventing new issues and all the opposite good things that occurs in a profitable wealthy nation financial system.

Till it went too far and we ended up with an excessive amount of cash chasing too few items – particularly homes. That led to a pattern of unacceptably quick Inflation, which we already coated in a current article.

So ultimately, Jay-P observed this and eased his foot again off of the Simple Cash Fuel Pedal. And naturally when rates of interest get jacked up, nearly every part else within the financial system slows down.

And that’s what is going on proper now: mortgages are immediately far more costly, so individuals are pushing aside their plans to purchase homes. Corporations discover that borrowing cash is expensive, so they’re scaling again their plans to construct new factories, and reducing again on their hiring. Fb laid off 10,000 individuals and Amazon shed 27,000.

We even had a miniature banking crisis the place some important mid-sized banks folded and gave the monetary world fears {that a} a lot greater set of dominoes would fall.

All of these items sound kinda dangerous, and should you make the error of checking the information, you’ll see there’s a massive dumb battle raging as common on each media outlet. Leftists, Proper-wingers, and anarchists all have a unique tackle it:

- It’s the President’s fault for printing all that cash and operating up the debt! We should always have Fiscal Self-discipline!

- No, it’s the other! The Fed is ruining the financial system with all these price rises, we have to drop them again down as a result of our poor center class is struggling!

- What are you two sheeple speaking about? The entire system is a bunch of corrupt cronies and we shouldn’t actually have a central financial institution. All hail the true world forex of Bitcoin!!!

The one factor all sides appear to agree on is that we’re “experiencing exhausting financial instances” and that “the nation is headed within the fallacious manner”.

Which, paradoxically, is totally fallacious as nicely – our unemployment price has dropped to 50-year lows and the financial system is on the absolute best it has ever been, a shock to even probably the most grounded economists.

The fact? We’re simply placing the lid again onto the ice cream carton till the financial system can digest all of the sugar it simply wolfed down. That is regular, it occurs each decade or two and it’s no massive deal.

Okay, however ought to I take my cash out of the inventory market as a result of it’s going to crash?

This reply by no means modifications, so that you’ll see it each time we discuss inventory investing: Holy Shit NO!!!

The inventory market all the time goes up in the long term, though with loads of unpredictable bumps alongside the way in which. Since you’ll be able to’t predict these bumps till after they occur, there’s no level in making an attempt to bop out and in of it.

However since we do take pleasure in hindsight, there are some things which have modified barely: From its peak in the beginning of 2022 till proper now (August 2023 as I write this), the general US market is down about 10%. Or to view it one other manner, it’s roughly flat since June 2021, so we’ve seen two years with no positive aspects other than whole dividends of about 3%.

For the reason that future is all the time the identical, unknowable factor, this implies I’m about 10% extra enthusiastic about shopping for my month-to-month slice of index funds at the moment than I used to be at these peak costs.

Ought to I begin placing cash into financial savings accounts as a substitute as a result of they’re paying 4.5%?

This can be a barely trickier query, as a result of in principle we must always put money into a logical, unbiased manner into the factor with the very best anticipated return over time.

When rates of interest have been underneath 1%, this was a straightforward choice: shares will all the time return excess of 1% over time – take into account the truth that the annual dividend funds alone are 1.5%!

However there must be some rate of interest at which you’d be keen to cease shopping for shares and like to only stash it into the steady, rewarding atmosphere of a cash market fund or long-term bonds or one thing else related. Proper now, if a good financial institution provided me, say, 12% I’d most likely simply begin loading up.

However keep in mind that the inventory market is additionally at the moment operating a ten% off sale. When the market ultimately reawakens and begins setting new highs (which it should sometime), any shares I purchase proper now can be value 10% extra. After which will proceed going up from there. Which rapidly turns into a good greater quantity than 12%.

In different phrases, the cheaper the shares get, the extra excited we must be about shopping for them fairly than chasing excessive rates of interest.

As you’ll be able to see, there isn’t a straightforward reply right here, however I’ve taken a center floor:

- I’m holding onto all of the shares I already personal, in fact

- BUT since I at the moment have an impressive margin loan stability for a home I helped to purchase with a number of mates (sure that is #3 in the previous couple of years!), I’m paying over 6% on that stability. So I’m directing all new revenue in the direction of paying down that stability for now, only for peace of thoughts and since 6% is an affordable assured return.

- Technically, I do know I’d most likely make a bit extra if I let the stability simply keep excellent, stored placing more cash into index funds, and paid the curiosity eternally, however this appears like a pleasant compromise to me

What if I need to Purchase a Home?

–

For many of us, the most important factor that rates of interest have an effect on is our choices round shopping for and promoting homes. Financing a house with a mortgage is immediately far more costly, any potential rental home investments are immediately far much less worthwhile, and conserving our outdated home with a locked-in 3% mortgage is immediately much more tempting.

Contemplate these stunning modifications simply over the previous two years as typical charges have gone from about 3% to 7.5%.

Assuming a purchaser comes up with the common 10% down fee:

- The month-to-month mortgage fee on a $400k home has gone from about $1500 in the beginning of 2022 final 12 months to roughly $2500 at the moment. Even scarier, the curiosity portion of that month-to-month invoice has greater than doubled, from $900 to $2250!

- For a house purchaser with a month-to-month mortgage finances of $2000, their outdated most home worth was about $500,000. With at the moment’s rates of interest nonetheless, that determine has dropped to about $325,000

- Equally, as a landlord in 2022 you may need been keen to pay $500k for a duplex which introduced in $4000 per 30 days of gross hire. At the moment, you’d must get that very same property for $325,000 to have the same web money move (or attempt to hire every unit for a $500 extra per 30 days) as a result of the curiosity price is a lot greater.

- And eventually, should you’re already residing in a $400k home with a 3% mortgage locked in, you might be successfully being backed to the tune of $1000 per 30 days by that success. In different phrases, you now have a $12,000 per 12 months disincentive to ever promote that home should you’ll must borrow cash to purchase a brand new one. And you’ve got a possible goldmine rental property, as a result of your carrying prices stay low whereas rents maintain going up.

This all sounds form of bleak, however sadly it’s the way in which issues are purported to work – the powerful drugs of upper rates of interest is meant to make the next issues occur:

- Home consumers will find yourself putting decrease bids which match inside their budgets.

- Landlords should be extra discerning about which properties to purchase up as leases, decreasing their very own bids as nicely.

- In the meantime, the present still-sky-high costs of housing ought to proceed to entice extra builders to create new houses and redevelop and improve outdated buildings and underused land, as a result of excessive costs imply good income. Then they’ll should compete for a thinner provide of residence consumers.

The web impact of all that is that costs ought to cease going up, and ideally fall again down in lots of areas.

When Will Home Costs Go Again Down?

This can be a difficult one as a result of the actual “worth” of a home relies upon completely on provide and demand. The suitable worth is no matter anyone is keen to pay for it. Nonetheless, there are a couple of fundamentals which affect this worth over the long term as a result of they decide the provide of housing.

- The precise price of constructing a home (supplies plus labor), which tends to only keep fairly flat – it may not even sustain with inflation.

- The worth of the underlying land, which must also comply with inflation on common, though with cold and warm spots relying on which cities are well-liked on the time.

- The quantity of bullshit which residents and their metropolis councils impose upon home builders, stopping them from producing the brand new housing that folks need to purchase.

The primary merchandise (building price) is fairly fascinating as a result of it’s topic to the magic of technological progress. Simply as TVs and computer systems get cheaper over time, home elements get cheaper too as issues like computerized manufacturing and world commerce make us extra environment friendly.

I bear in mind paying $600 for a fancy-at-the-time undermount sink and $400 for a faucet for my first kitchen rework within the 12 months 2001. At the moment, you may get a nicer sink on Amazon for about $250 and the tap is a flat hundred. Equally, nailguns and cordless instruments and easy-to-install PEX plumbing make the method of constructing quicker and simpler than ever.

Alternatively, the final merchandise (bullshit restrictions) has been very inflationary in current instances. I’ve observed that yearly one other layer of purple tape and complex codes and onerous zoning and approval processes will get layered into the native e book of guidelines, and consequently I simply gave up on constructing new homes as a result of it wasn’t well worth the problem. Different builders with extra endurance will proceed to plow by the murk, however they are going to have much less competitors, fewer permits can be granted, and thus the scarcity of housing will proceed to develop, which raises costs on common.

Fortunately, each metropolis is completely different and a few have chosen to make it simpler to construct new homes fairly than harder. Even higher, locations like Tempe Arizona are permitting good housing to be constructed round people rather than cars, which is much more inexpensive to assemble.

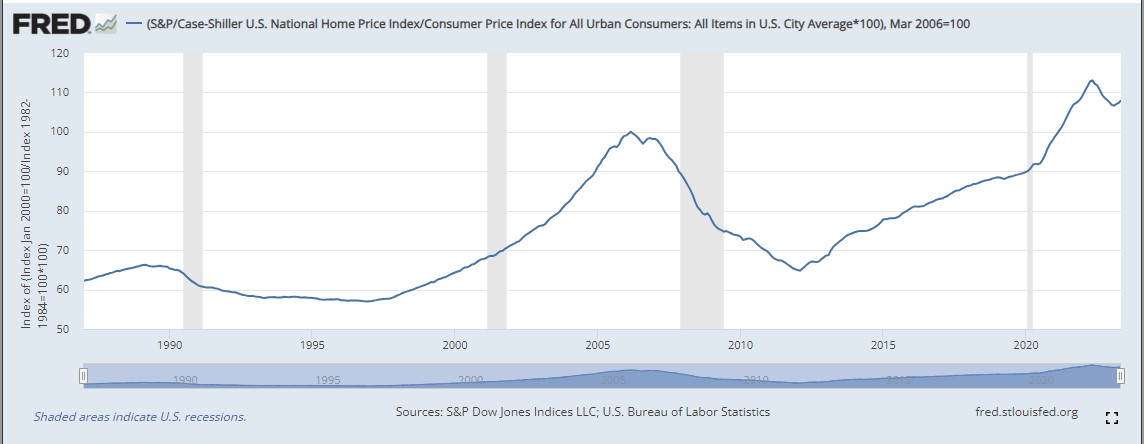

However general, since general US home costs adjusted for inflation are nearly at an all-time excessive, I feel there’s an opportunity that they may ease again down one other 25% (to 2020 ranges). However who is aware of: my guess might show completely fallacious, or the “fall” might simply come within the type of flat costs for a decade that don’t sustain with inflation, that means that they simply really feel 25% cheaper relative to our greater future salaries.

When Will Curiosity Charges Go Again Down?

The humorous half about our present “excessive” rates of interest is that they aren’t truly excessive in any respect. They’re proper round common.So they won’t go down in any respect for a very long time.

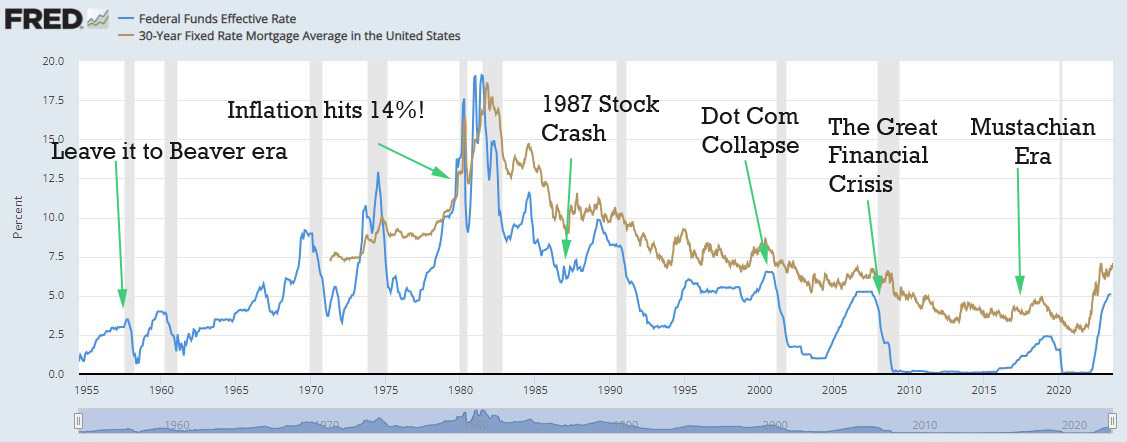

Keep in mind that graph in the beginning of this text? I intentionally cropped it to indicate solely the years since 2009 – the lengthy current interval of low rates of interest. However should you zoom out to cowl the final seventy years as a substitute, you’ll be able to see that we’re nonetheless in a really regular vary.

–

However a greater reply is that this one: Rates of interest will go down each time Jerome Powell or one in every of his successors determines that our financial system is slowing down an excessive amount of and desires one other hit from the fuel pedal. In different phrases, each time we begin to slip into a real recession.

To be able to do this nonetheless, we have to see low inflation, rising unemployment, and different indicators of an financial system that’s lastly cooling down. And proper now, these issues maintain not displaying up within the weekly financial knowledge.

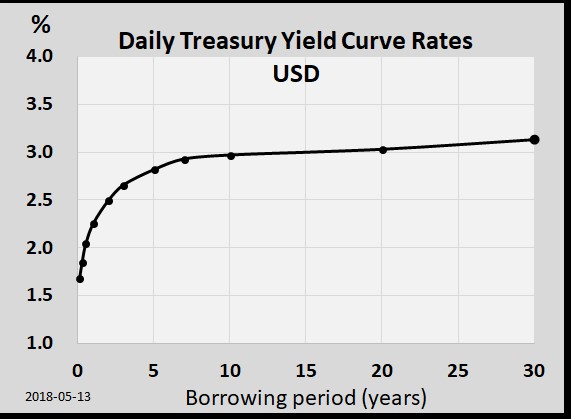

You will get one affordable prediction of the way forward for rates of interest by one thing referred to as the US Treasury Yield Curve. It sometimes appears to be like like this:

–

What the graph is telling you is that as a lender you get an even bigger reward in change for locking up your cash for an extended time interval. And manner again in 2018, the individuals who make these loans anticipated that rates of interest would common about 3.0 % over the subsequent 30 years.

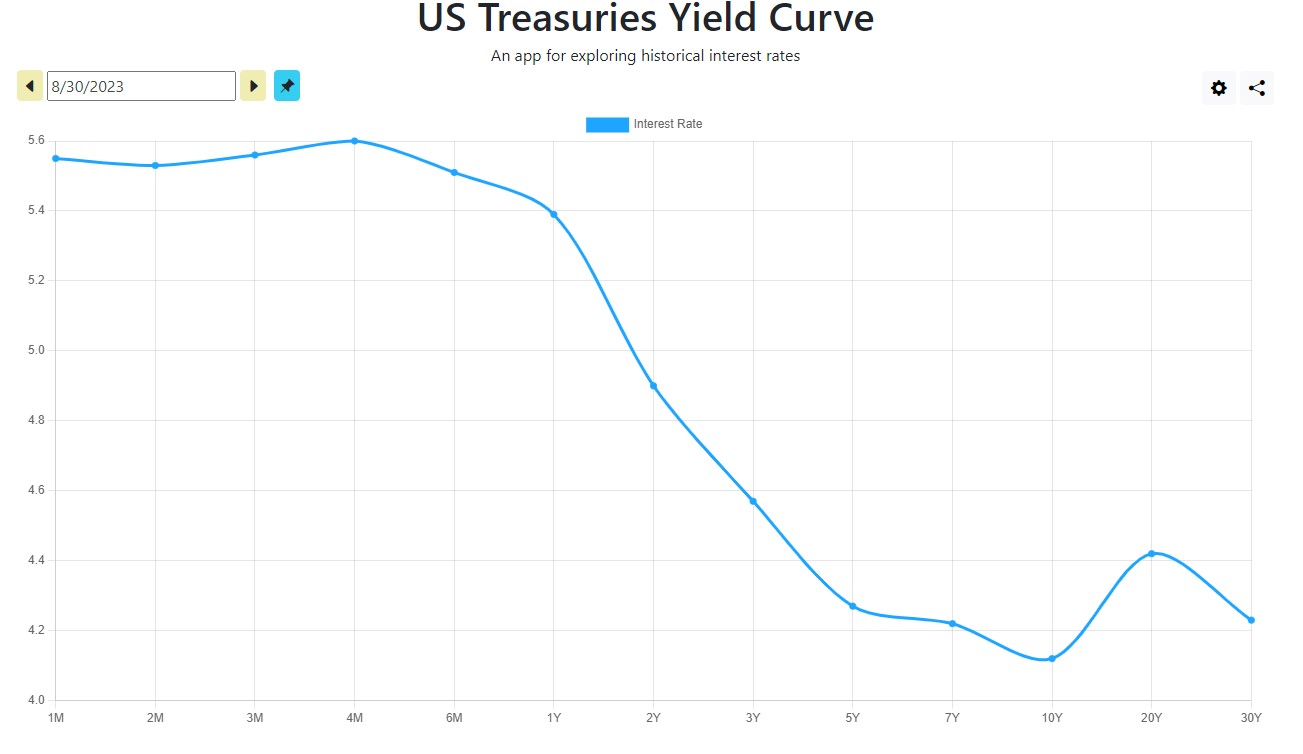

At the moment, we have now a really unusual reverse yield curve:

–

If you wish to lend cash for a 12 months or much less, you’ll be rewarded with a juicy 5.4 % rate of interest. However for 2 years, the speed drops to 4.92%. After which ten-year bond pays solely 4.05 %.

This example is bizarre, and it’s referred to as an inverted yield curve. And what it means is that the consumers of bonds at the moment imagine that rates of interest will nearly actually drop sooner or later – beginning slightly over a 12 months from now.

And should you recall our earlier dialogue about why rates of interest drop, because of this traders are forecasting an financial slowdown within the pretty close to future. And their instinct on this division has been fairly good: an inverted yield curve like this has solely occurred 11 instances up to now 75 years, and in ten of these circumstances it precisely predicted a recession.

So the quick reply is: no one actually is aware of, however only for enjoyable I’ll make a guess. Then if I’m fallacious in public, you’ll be able to come again and make enjoyable of this within the feedback.

I feel we’ll most likely see rates of interest begin to drop inside 18-24 months, and the occasion could also be accompanied by some form of recession as nicely.

The Final Curiosity Price Technique Hack

–

I prefer to learn and write about all these items as a result of I’m nonetheless a finance nerd at coronary heart. However when it comes right down to it, rates of interest don’t actually have an effect on long-retired individuals like many people MMM readers, as a result of we’re largely accomplished with borrowing. I just like the simplicity of proudly owning only one home and one automotive, mortgage-free.

With the present overheated housing market right here in Colorado, I’m not tempted to even take a look at different properties, however sometime which will change. And the wonderful thing about having precise financial savings fairly than only a excessive revenue that allows you to qualify for a mortgage, is which you could be able to pounce on an excellent deal on quick discover.

Perhaps your complete housing market will go on sale as we noticed within the early 2010s, or maybe only one good property within the mountains will come up on the proper time. The purpose is that when you’ve got sufficient money to purchase the factor you need, the rates of interest that different individuals are charging don’t matter. It’s a pleasant place of power as a substitute of stress. And you’ll nonetheless determine to take out a mortgage should you do discover the charges are worthwhile to your personal objectives.

So to tie a bow on this complete lesson: maintain your life-style lean and joyful and don’t lose an excessive amount of sweat over at the moment’s rates of interest or home costs. They are going to most likely each come down over time, however these issues aren’t in your management. Way more essential are your personal selections about incomes, saving, wholesome residing and the place you select to dwell.

With these massive sails of your life correctly in place and pulling you forward, the smaller problems with rates of interest and no matter else they write about within the monetary information will regularly shrink right down to turn into simply ripples on the floor of the lake.

Within the feedback: what have you ever been serious about rates of interest lately? Have they modified your choices, elevated, or even perhaps decreased your stress ranges round cash and housing?

—

* Picture credit score: Mr. Cash Mustache, and Rustoleum Extremely Cowl semi gloss black spraypaint. I initially polled some native mates to see if anybody owned costume footwear and a swimsuit so I might get this image, with no luck. So I painted up my outdated semi-dressy footwear and located some clean-ish black socks and pants and vacuumed out my automotive a bit earlier than taking this image. I’m kinda pleased with the outcomes and it saved me from hiring Jerome Powell himself for the shoot.

[ad_2]

Source link

{kind=link}

{kind=link}