Effectively, that was kinda sudden!

Within the three months or so since we final spoke, the world has turn out to be a completely completely different place – at the very least for these of us who sustain with any kind of worldwide, monetary or inventory market information.

The headlines are new, and the issues are after all very actual. Russia has began one of many largest, shittiest wars in a era – killing untold hundreds of individuals, displacing hundreds of thousands, and halting trillions of {dollars} of manufacturing and commerce. This has compounded the “all the things scarcity” of damaged provide chains that we’ve got all been feeling for the previous two years, creating much more inflation particularly in oil costs. And simply to amplify all the things even additional, China has launched a batshit loopy (and medically inconceivable) “zero covid” coverage, locking down a whole lot of hundreds of thousands of its personal individuals who can not produce or export the issues that the remainder of the world’s financial system had grown to depend upon.

The ensuing scarcity of products and employees has created rising costs (inflation), which has triggered our central bankers to lastly rise from their slumber and begin jacking up rates of interest.

Which has in flip triggered the extra skittish inventory traders to run for the exits and fully change their view of our financial future, flooding the monetary information with pink ink and scary headlines.

The underside line is that the general US inventory market is down about 20% over the previous three months. Which signifies that in case you add up your internet value as I do sometimes, chances are you’ll discover that just about a fifth of it has all of the sudden gone up in smoke.

Happily, that is simply an phantasm. Whereas the human facet of each struggle is terrible and you need to assist out in case you can, the monetary facet of this panic could be very regular and we had been overdue for one thing like this to occur.

A 20% drop in inventory costs is known as a “bear market” they usually historically occur each few years, lasting simply 9 months or so from prime to backside. However within the Mustachian Period (the years since 2011 after I started writing this blog), there has solely been one: the 2020 Covid Crash which solely lasted a couple of month. Heck, even in my 25 12 months investing lifetime (roughly 1997 to current), there have solely been a handful:

| Bear market date | Decline (peak to trough) | Length (months) |

| March 2000 – Sept 2001 (dotcom bust) | -36% | 18 |

| Jan – October 2002 (extra dotcom+housing) | -34% | 9 |

| Oct 2007-Nov 2008 (nice monetary disaster) | -52% | 14 |

| Jan – Mar 2009 (extra GFC) | -28% | 2 |

| Feb-March 2020 (covid crash) | -34% | 1 |

| April 2022 – ??? (the present blowup) | -20% to this point | What’s your guess? |

.

So in case you’re below 40, a few of this may increasingly really feel unfamiliar.

Now that we’ve lined the background, we will get into some higher information:

- That is all a standard, wholesome a part of the financial cycle. The truth is, our central bankers have intentionally created this case in your personal good they usually most likely ought to have completed it a 12 months in the past.

- If you’re nonetheless shopping for or holding shares (versus actively promoting them), this inventory market crash is definitely making you richer

- Even in case you are retired and dwelling completely off of your investments, inventory market declines are to be anticipated and shouldn’t derail your lifetime of leisure – so long as you might be following a tough approximation of the 4% rule and stay versatile and perceive the idea of a Safety Margin.

If you happen to actually perceive the factors above and actually really feel excited about them, you may drop the concern and stress out of your investing life, which suggests you’ll reside a life that’s each wealthier, and extra enjoyable. So let’s cowl every level correctly, so that you may be enthusiastic about all this as I’m.

1) Why is that this wholesome once more?

First, the half in regards to the Federal Reserve and why a central banking system is so helpful (regardless of the claims of monetary anarchists like Bitcoin lovers):

When one thing dangerous occurs (just like the sudden deliberate recession we brought about resulting from our personal 2020 Covid shutdowns), the Fed can drop rates of interest and “print cash” in different methods to spice up funding and demand within the financial system. And it really works – because of this our financial system bounced again so shortly from the biggest slowdown in historical past.

Some may say it labored too properly – whereas we’ve got benefited from file low unemployment, we’ve got additionally seen costs of homes, shares, and all the things else rise with alarming pace. So finally, they needed to flip off the booster.

By elevating rates of interest, the central bankers put a slight drag on enterprise spending, client borrowing and inventory market exuberance. This lowers demand for all the things, which pours some chilly water on inflation. The deflating of essentially the most overpriced shares reveals that the coverage is working. And over the following 12 months, increased mortgage charges also needs to finish the loopy bidding struggle of a housing market we’ve been seeing in most cities.

However inventory market crashes and even temporary recessions are good for extra than simply combating inflation. They’re good for combating a persistent flaw in human nature itself.

People are lazy creatures at coronary heart. When issues get too straightforward, we lose our edge and our motivation to be taught, innovate and make adjustments. It occurs on the particular person stage, as I discover after I waste sure evenings on the sofa engaging in nothing. And it occurs much more within the collective sense, if a gaggle of individuals secures a pleasant stream of energy and revenue that continues to be unchallenged.

Think about that you just’re operating an organization. Your clients maintain shopping for your stuff it doesn’t matter what you do, traders bid your inventory worth as much as the moon no matter your monetary efficiency, and there’s no competitors on the horizon. What do you assume will occur to your monopoly?

There’s no want to take a position on this, as a result of it has occurred to various levels for the reason that starting of financial time. The reply is that you begin to suck. Your product innovation stagnates, your clients develop much less and fewer glad, and your traders develop nervous. Finally, one thing comes alongside to poke at this bubble of complacency – on this case struggle and covid and inflation – after which POP! – your gross sales dry up, your inventory worth crashes, and your cozy company desk has become a tattered garden chair within the parking zone and your small business is finished.

However wait! Whilst you had been including that closing layer of lipstick to your out of date movie digicam or guide typewriter or gasoline-powered line of vehicles and vans, there really had been opponents on the market, inventing higher merchandise and providing higher customer support and conserving their steadiness sheets lean, as a result of they needed to, as a result of issues for them had been onerous.

Your inefficient firm goes out of enterprise, and your extra nimble opponents welcome your former clients. They might even suck up the very best of your former staff and purchase your outdated manufacturing unit to start out making new, higher merchandise.

This occurs on a regular basis, and whereas it may be painful for many who weren’t ready, it’s a wholesome factor for enterprise total. And a wholesome factor for overpriced housing markets, and the speculatively inflated costs of oil, lumber, copper and all the things else.

To a sure extent, the excessive costs had been helpful in sending a sign that we have to produce extra of these items. However past that restrict, folks began shopping for overpriced shares, homes, cryptocoins and commodities just because they hoped to make a fast buck by flipping them to another person at a better worth. As a substitute of investing in a productive asset, these speculators had been simply assuming the latest momentum would proceed. The sort of playing is a waste of everybody’s time, and a very good worth crash is the way in which we flush the monetary rest room.

2) My internet value has simply cratered by 20%. How precisely does this imply I get richer?

The very first thing to ask your self is, “20% of what?”

Certain, inventory costs are down from a latest peak, however that peak itself was simply an arbitrary fleeting second of investor enthusiasm. Was that earlier worth actually the “proper” worth for shares, or did you simply develop connected to it due to our recognized human weak spot of Loss Aversion?

To place it one other method, what if as a substitute of our investments because the monetary media likes to painting them, which is like this:

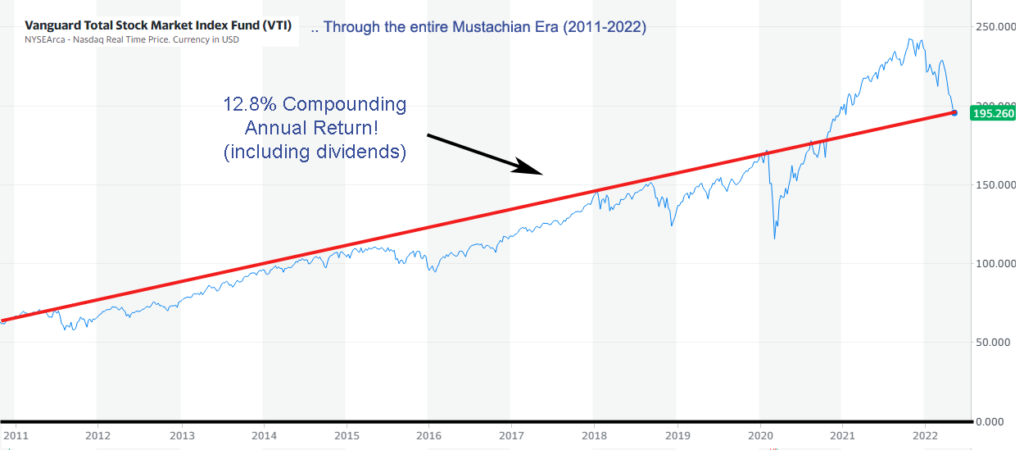

What if we determined to be extra wise, begin the damned Y axis at zero as each graph ought to do, and zoom out to an inexpensive time horizon,such because the Age of Mustachianism which occurred to start in 2011. And ignore the wiggly blue line and observe the extra significant pink line.

Effectively, how fascinating. Not solely has this crash returned us to a roughly straight line of long term inventory market development, however that line itself is very beneficiant, representing a 12.8% annual compound achieve in case you think about a quarterly reinvestment of dividends (which usually add about 2% to your annual returns however aren’t proven in these charts). Over longer durations like 50 years, inventory returns have been nearer to 10% after dividends, which suggests we’ve nonetheless had greater than our share of fine instances.

Within the lengthy return, inventory costs are decided by this system:

Inventory worth = firm earnings x BRM*

*(Bullshit Random Multiplier)

The BRM, extra formally generally known as the Worth-to-Earnings ratio or P/E, is meant to be primarily based on a mathematical estimate of the current worth of all future dividends you’ll obtain in case you maintain a inventory for your entire lifetime of the corporate.

Once we anticipate increased rates of interest or inflation over the following 20 years, the P/E ought to fall as a result of these distant future earnings turn out to be value much less in right now’s {dollars}. In the meantime, if we someway understand that the long-term way forward for the enterprise world is much more rosy than we thought, the P/E ought to rise as a result of traders can precisely predict a bigger stream of future earnings.

However the “bullshit” issue is available in resulting from issues just like the “He Mentioned She Mentioned” nature of no matter Elon posted on Twitter right now, momentum buying and selling algorithms, meme inventory merchants banding collectively to drive up random shares no matter underlying worth, and extra. Briefly, the brief time period BRM is only a measure of the current second’s steadiness of greed and concern.

As an investor, nevertheless, you don’t care in regards to the BRM. The truth is, you don’t even actually care in regards to the share costs of your investments, as a result of the worth of a person share solely issues twice in your lifetime:

- The second you purchase it,

- And the second you promote it.

The whole lot else is simply foolish noise.

Proper now, most of us are nonetheless incomes cash and accumulating extra shares. Even Mr. Cash Mustache, as an individual who retired 17 years in the past, continues to be on this boat for the straightforward cause that my retirement revenue from dividends and pastime companies continues to be better than my annual dwelling bills (which nonetheless hover round $20,000 per 12 months).

On prime of this, in case you are holding principally index funds as you have to be, your shares ship a pleasant serving to of dividends each three months, which you could have set to routinely reinvest into nonetheless extra shares of those self same index funds. In right now’s market, you might be getting about 25% extra shares for every greenback that you just make investments. Which interprets to a full 25% extra wealth from these shares in your future.

(It’s enjoyable math – a 20% drop in costs means you get 25% extra shares in your greenback, and a 50% drop means twice as many, or 100% extra shares per greenback invested.)

3) Okay, however I actually am retired and attempting to reside off my investments now. How is that this not a catastrophe for me?

To begin with, you’re nonetheless getting the dividends that we celebrated in level 2) above. When the inventory market crashes, dividend funds often stay way more steady as a result of the massive, established firms in your index funds proceed to become profitable.

It’s fairly much like proudly owning a portfolio of rental homes unfold all through the world: whereas home costs fluctuate on a regular basis in several cities, the full hire paid by a gaggle of hundreds of tenants will have a tendency to stay fairly steady and simply rise on the charge of inflation.

So this stream of cash will maintain coming in and masking a considerable portion of your dwelling bills (between 30% and 50% for many retirees in right now’s market circumstances in case you retired utilizing the 4% rule).

Even in case you don’t alter your spending or revenue throughout this bear market, the top result’s that you just must promote a tiny proportion of your shares at a reduction throughout the bear market – which suggests your portfolio shrinks a bit quicker.

However the 4% rule already takes this under consideration: if there have been no such factor as bear markets, the secure withdrawal charge would really be equal to the long-term common of inventory market development, which is nearer to 7% after inflation. By sticking to 4% or barely much less, you might be giving your self a excessive likelihood of weathering the storm.

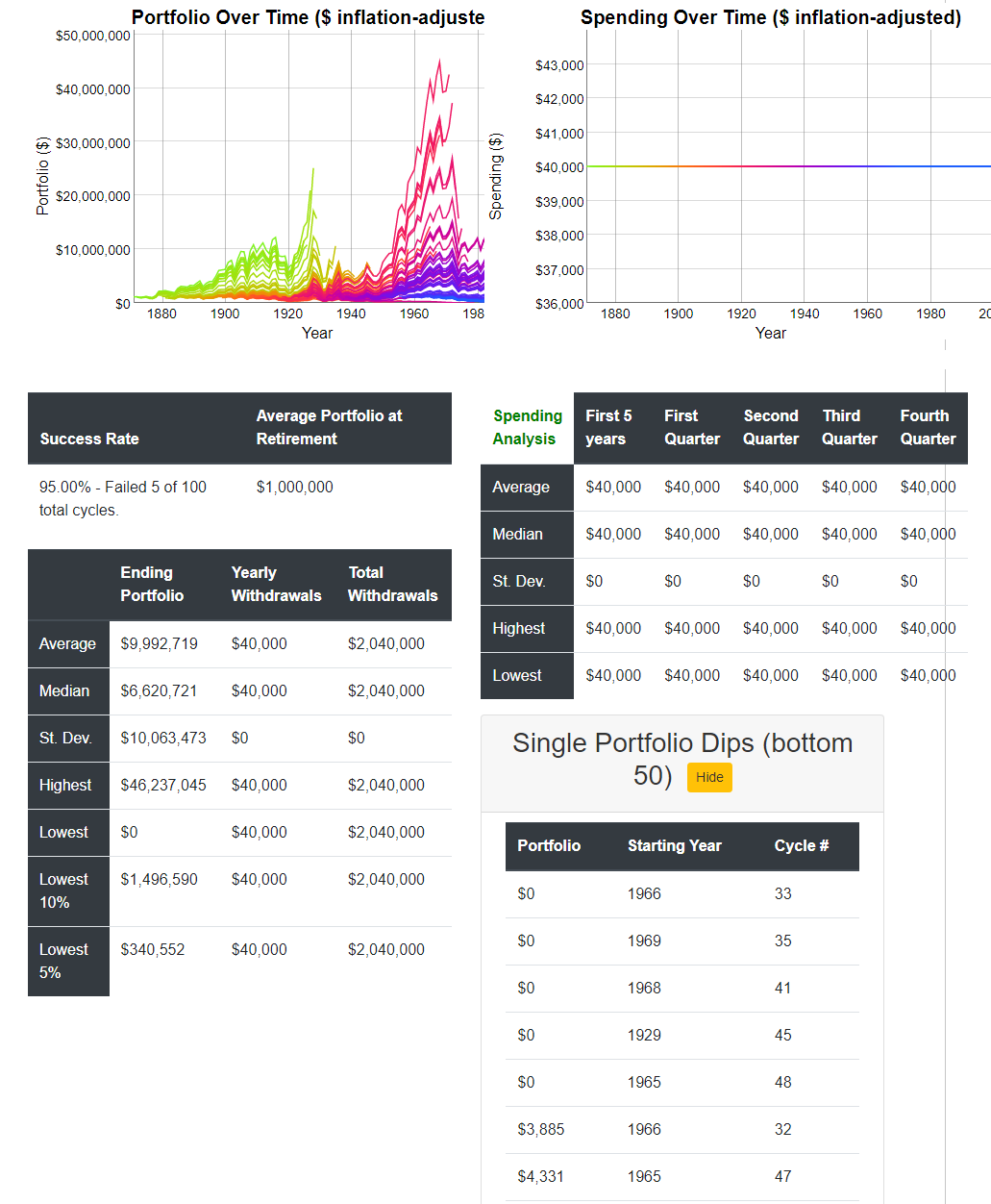

cFireSim: Financial Historical past to the Rescue!

Assuming a small $1k enhance from social safety in my 60s, I’d have a 95% historic success charge. Solely the Nice Melancholy and the Nineteen Sixties stoop would have foiled this plan, and even then simply barely.

To essentially perceive what this implies I reached out to Lauren Boland, the monetary calculations wizard behind the wonderful cFireSim retirement simulator. Her long-running web site offers you the very best shot at answering the query: “If I retire with a set chunk of cash, what are my possibilities of success?”

I requested her what it actually means when the inventory market drops: does a 20% drop actually make you 20% much less “retired” or is precise final result extra delicate? True to type, she acquired again to me inside only a few minutes with these ideas:

MMM: How ought to potential retirees consider the latest crash in valuation – has it actually pushed out their retirement date, or not?

Lauren:

It depends upon how versatile you might be keen to be along with your spending. As shares get costlier (a better price-to-earnings ratio), it may be an ideal time to spend extra (take these positive factors), and after they drop in worth (like proper now), chances are you’ll need to spend much less to protect your capital.

Now we have a reputation for the this concept of inventory crashes that come at simply the fallacious time: the Sequence of Returns Threat. If you happen to retire simply BEFORE a giant inventory market crash, your first few months or years will drain your portfolio a bit greater than you anticipated, till inventory costs get well. So, latest retirees reside this proper now in the event that they retired with out a lot security margin.

Then again, If you happen to HAVEN’T retired but, and your numbers nonetheless look good even now, I feel it could really be a greater time to retire, since you may hope that historical past repeats itself and there’s a restoration. It’d be like retiring on the backside of 2009 with still-decent numbers.

— (thanks Lauren!) —

Okay, so we’re most likely not screwed both method. However nonetheless, as a Mustachian this looks as if a nice excuse to check with level #1 above: use the chaos and disruption as an excuse to make your self stronger. Turn into extra environment friendly along with your spending, discover fulfilling methods to create worth for others that occur to provide cash for you as properly, and enhance your train, consuming and private development packages as properly. As a result of hey, why not?

Epilogue: How does all this Distress finish?

Though you now perceive that even the present state of affairs is regular and wholesome, there may be even higher information on the core of it: It’s a self-correcting drawback, and the answer is already within the works.

A scarcity of products, a sloshing overflow of the cash provide and inappropriately low rates of interest led to all the things getting costlier. However in the meantime, firms have constructed extra factories and employed extra employees to extend manufacturing and now the central banks have cranked up rates of interest and reversed their different help packages as properly.

The end result: mortgages value extra so housing gross sales have slowed. Customers and companies are each pissed off by latest worth will increase and extra cautious in regards to the future so they’re shopping for much less stuff, which reduces the The whole lot-Scarcity that we talked about earlier. All of a sudden, provide catches as much as demand and costs cease rising.

Or to summarize all of this in a a lot pithier method: the answer to excessive costs, is excessive costs.

The world is frightening and the inventory market has plunged, however the elementary image hasn’t modified in any respect: billions of people are working onerous and making use of their ingenuity every single day to get forward. It’s a messy course of, however on common we proceed to succeed at this process over time. Individuals who perceive this unchanging mechanism will have a look at this 12 months’s sale on productive asset and say, “Cool – signal me up for one more serving to of future wealth, and thanks for the deal!”

Within the feedback – what are YOU doing in response to this bear market? Are you scared, or doubling down on investing?

{kind=link}

{kind=link}